Even for people familiar with the responsible investment industry, ESG (environmental, social and governance) can mean different things – and it is often pursued for different reasons.

The best place to start is to understand that all of these terms describe ‘value-based investing’, ‘values-based investing’, or something in between.

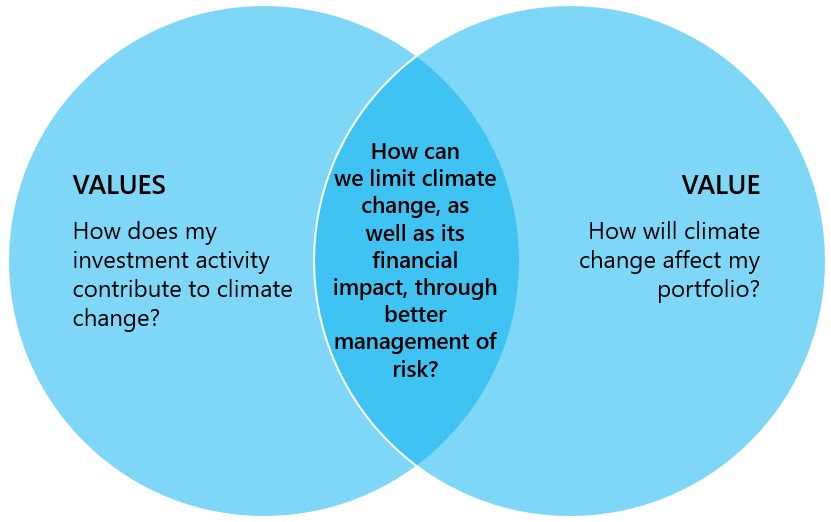

- Values-based investing means including extra (‘moral’ or ‘ethical’ related) rules when investing. It can include restricting decision making or limiting the investible universe based on a set of values, or using an investment process that gives these factors extra weight. Screening (ethical screens), divesting and tilting all fall into this category.

- Value-based investing uses some of the same social or environmental information as values-based investing, but does so within its ordinary investment process to improve performance. In essence, it uses insights on ESG performance to gather a more complete picture of a business’s value drivers and to make better predictions about how it will perform financially over the longer term. ESG integration into core investment processes is the most common value-based approach.

Applying values to investment decisions – expressing matters of conscience

Expressing values through investing has a long history, thanks to religious groups wanting investments that conform to the rules of their faiths. Many religious investors continue to avoid holding shares in companies that make profits from alcohol, gambling, lending money at interest, or stem cell research, for example.

Today, there are many non-religious reasons why individuals wish to express values through investments. Often these decisions are shaped by environmental and humanitarian concerns. For instance, some may wish to exclude companies which cause harm (e.g. weapons manufacturers), while others might seek out those companies which are seen to contribute to society (e.g. health care, renewable energy).

Improving investment performance – understanding the impact on long term value

The idea that environmental, social and corporate governance (ESG) analysis can improve investment performance is newer. It has grown with the realisation that on average 50% of the underlying value of a company today is attributable to intangible value. Another way to think about this is the “invisible infrastructure” a company relies on to operate and grow: its brand and reputation, its culture and ingenuity, how efficiently it is organised for effective risk management.

Markets are not as good at processing qualitative information; that’s why many consider a value-based approach to be a competitive advantage. For instance, share prices often get a sudden boost when a company announces lay-offs, ignoring the impact on future performance when fewer staff means unhappier customers, sluggish innovation, and problems with products or compliance. A company’s impact on employees, local communities or the environment can mean future profits are hampered by a poor reputation affecting sales, regulatory constraints, or problems in securing funding.

Consider whether values or value is driving the investment

Regardless of what labels are used, it is important to be able to identify whether a product is delivering a values-based or a value-based approach (or doing each partially) – to avoid any unwanted surprises.

A quick test for quality where there is a values-based approach is asking how independent are any investment rules from a financial or business case. This makes it possible to evaluate the values being addressed for their goodness of fit for a given situation.

A test for quality in products that emphasise value is asking how strong is the business/investment case that links social or environmental information to the investment decision. If it is to deliver on investment performance, it needs to be robust.

The opinions expressed in this content are those of the author shown, and do not necessarily represent those of No More Practice Education Pty Ltd or its related entities. All content is intended for a professional financial adviser audience only and does not constitute financial advice. To view our full terms and conditions, click here.